Workshop 06 Accounting for Income Taxes

Question 9

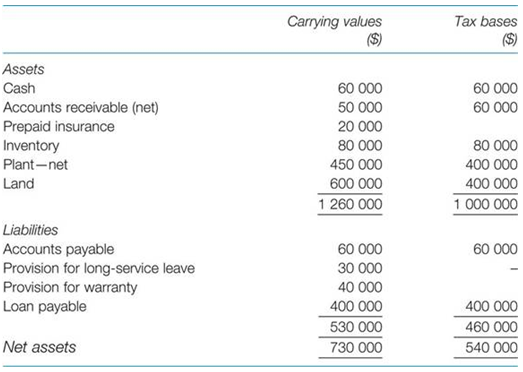

Boiling Pot Limited commences operations on 1 July 2018. One year after the commencement of its operations (30 June 2019) the entity prepares the following information, showing both the carrying amounts for accounting purposes and the tax bases of the respective assets and liabilities.

Other information

After adjusting for differences between tax rules and accounting rules, it is determined that the taxable income of Boiling Pot Limited is $700 000.

There is a doubtful debt provision of $10 000.

An item of plant is purchased at a cost of $600 000 on 1 July 2018. For accounting purposes it is expected to have a life of four years; however, for taxation purposes it can be depreciated over three years. It is not expected to have any residual value.

Boiling Pot Limited has some land, which cost $400 000 and which has been revalued to its fair value of $600 000 in accordance with AASB 116.

None of the amounts accrued in respect of warranty expenses or long-service leave has actually been paid.

The tax rate is 30 per cent.

Required:

(a) Complete the taxation worksheet in accordance with AASB112.

(b) Prepare the applicable journal entries to record tax adjustments.

Question 10

La Trobe Ltd commences operations on 1 July 2018. One year later, on 30 June 2019, the entity prepares the following information, showing both the carrying amounts for accounting purposes, and tax bases of the respective assets and liabilities.

Other Information:

The accounting profit before tax for the year was $285,000 (for the year 2019).

There is a doubtful debt provision of $5,000.

An item of plant is purchased at a cost of $200,000 on 1 July 2018. For accounting purposes, it is expected to have a life of 5 years; however, for taxation purposes it can be depreciated over 4 years. It is not expected to have any residual value.

The amount accrued in respect of warranty expenses was paid on 31 July 2019. Long service leave has not been paid.

The tax rate is 30 percent.

Required:

Prepare the tax reconciliation statement for the year ended 30 June 2019, the related deferred tax worksheet and journal entries to recognise deferred tax.

Workshop 07 and 08 Accounting for Group Structures

Question 11 (updated 3/6/2020)

(a) What are the rationales for consolidating the accounts of different legal entities?

(b) Tamarama Ltd acquires 100 per cent of Bronte Ltd on 1 July 2017. Tamarama Ltd pays the shareholders of Bronte Ltd the following:

Cash $70,000

Plant and equipment Market value $250,000; carrying amount in the books of Tamarama Ltd $170,000

Land Market value $300,000; carrying amount in the books of Tamarama Ltd $200,000

There are also legal fees of $35,000 involved in acquiring Bronte Ltd.

On 1 July 2017 Bronte Ltd’s statement of financial position shows total assets of $700 000 and liabilities of $300 000. The fair value of the assets is $800 000.

REQUIRED

Has any goodwill been acquired and, if so, how much?

Question 12

The following financial statements of Mungo Ltd and its subsidiary Barry Ltd have been extracted from their financial records at 30 June 2019.

Other information

• Mungo Ltd acquired its 100 per cent interest in Barry Ltd for $712 000 on 1 July 2018, that is four years earlier. At that date the capital and reserves of Barry Ltd were:

Share capital $400000

Retained earnings $250000

$650000

At the date of acquisition all assets were considered to be fairly valued.

• During the year Mungo Ltd made total sales to Barry Ltd of $130 000, while Barry Ltd sold $104 000 in inventory to Mungo Ltd.

• The closing inventory in Mungo Ltd includes inventory acquired from Barry Ltd at a cost of $67 200. This cost Barry Ltd $52 000 to produce.

• The closing inventory of Barry Ltd includes inventory acquired from Mungo Ltd at a cost of $24 000. This cost Mungo Ltd $19 200 to produce.

• The management of Mungo Ltd believe that goodwill acquired was impaired by $5000 in the current financial year.

• Barry Ltd paid $20 000 in management fees to Barry Ltd.

• The tax rate is 30 per cent.

Required:

Provide the consolidated journal entries for Mungo Ltd and Barry Ltd as at 30 June 2019.

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

Login | Sign Up

Login | Sign Up