22-18 Benefits and costs of decentralization.

Jackson Markets, a chain of traditional supermarkets, is interested in gaining access to the organic and health food retail market by acquiring a regional company in that sector. Jackson intends to operate the newly acquired stores independently from its supermarkets.

One of the prospects is Health Source, a chain of 20 stores in the mid-Atlantic region. Buying for all 20 stores is done by the company’s central office. Store managers must follow strict guidelines for all aspects of store management in an attempt to maintain consistency among stores. Store managers are evaluated on the basis of achieving profit goals developed by the central office.

The other prospect is Harvest Moon, a chain of 30 stores in the Northeast. Harvest Moon managers are given significant flexibility in product offerings, allowing them to negotiate purchases with local organic farmers. Store managers are rewarded for exceeding self-developed return-on-investment goals with company stock options. Some managers have become significant shareholders in the company and have even decided on their own to open additional store locations to improve market penetration. However, the increased autonomy has led to competition and price cutting among Harvest Moon stores within the same geographic market, resulting in lower margins.

Required:

1. Would you describe Health Source as having a centralized or a decentralized structure? Explain.

2. Would you describe Harvest Moon as having a centralized or a decentralized structure? Discuss some of the benefits and costs of that type of structure.

3. Would stores in each chain be considered cost centers, revenue centers, profit centers, or investment centers? How does that tie into the evaluation of store managers?

4. Assume that Jackson chooses to acquire Harvest Moon. What steps can Jackson take to improve goal congruence between store managers and the larger company?

22-19 Transfer-pricing methods, goal congruence.

British Columbia Lumber has a raw lumber division and a finished lumber division. The variable costs are as follows:

Raw lumber division: $100 per 100 board-feet of raw lumber

Finished lumber division: $125 per 100 board-feet of finished lumber

Assume that there is no board-feet loss in processing raw lumber into finished lumber. Raw lumber can be sold at $200 per 100 board-feet. Finished lumber can be sold at $275 per 100 board-feet.

Required:

1. Should British Columbia Lumber process raw lumber into its finished form? Show your calculations.

2. Assume that internal transfers are made at 110% of variable cost. Will each division maximize its division operating-income contribution by adopting the action that is in the best interest of British Columbia Lumber as a whole? Explain.

3. Assume that internal transfers are made at market prices. Will each division maximize its division operating-income contribution by adopting the action that is in the best interest of British Columbia Lumber as a whole? Explain.

22-20 Multinational transfer pricing, effect of alternative transfer-pricing methods, global income tax minimization.

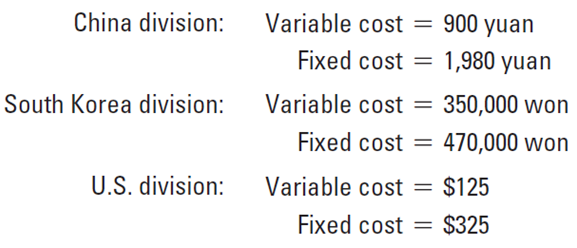

Tech Friendly Computer, Inc., with headquarters in San Francisco, manufactures and sells a desktop computer. Tech Friendly has three divisions, each of which is located in a different country:

a. China division—manufactures memory devices and keyboards

b. South Korea division—assembles desktop computers using locally manufactured parts, along with memory devices and keyboards from the China division

c. U.S. division—packages and distributes desktop computers

Each division is run as a profit center. The costs for the work done in each division for a single desktop computer are as follows:

Chinese income tax rate on the China division’s operating income: 40%

South Korean income tax rate on the South Korea division’s operating income: 20%

U.S. income tax rate on the U.S. division’s operating income: 30%

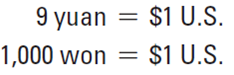

Each desktop computer is sold to retail outlets in the United States for $3,800. Assume that the current foreign exchange rates are as follows:

Both the China and the South Korea divisions sell part of their production under a private label. The China division sells the comparable memory/keyboard package used in each Tech Friendly desktop computer to a Chinese manufacturer for 4,500 yuan. The South Korea division sells the comparable desktop computer to a South Korean distributor for 1,340,000 won.

Required:

1. Calculate the after-tax operating income per unit earned by each division under the following transfer-pricing methods: (a) market price, (b) 200% of full cost, and (c) 350% of variable cost. (Income taxes are not included in the computation of the cost-based transfer prices.)

2. Which transfer-pricing method(s) will maximize the after-tax operating income per unit of Tech Friendly Computer?

22-21 Effect of alternative transfer-pricing methods on division operating income.

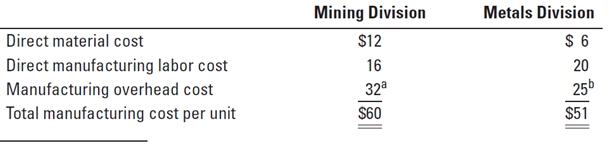

(CMA, adapted) Ajax Corporation has two divisions. The mining division makes toldine, which is then transferred to the metals division. The toldine is further processed by the metals division and is sold to customers at a price of $150 per unit. The mining division is currently required by Ajax to transfer its total yearly output of 200,000 units of toldine to the metals division at 110% of full manufacturing cost. Unlimited quantities of toldine can be purchased and sold on the outside market at $90 per unit.

The following table gives the manufacturing cost per unit in the mining and metals divisions for 2014:

a. Manufacturing overhead costs in the mining division are 25% fixed and 75% variable.

b. Manufacturing overhead costs in the metals division are 60% fixed and 40% variable.

Required:

1. Calculate the operating incomes for the mining and metals divisions for the 200,000 units of toldine transferred under the following transfer-pricing methods: (a) market price and (b) 110% of full manufacturing cost.

2. Suppose Ajax rewards each division manager with a bonus, calculated as 1% of division operating income (if positive). What is the amount of bonus that will be paid to each division manager under the transfer-pricing methods in requirement 1? Which transfer-pricing method will each division manager prefer to use?

3. What arguments would Brian Jones, manager of the mining division, make to support the transfer-pricing method that he prefers?

22-22 Transfer pricing, general guideline, goal congruence.

(CMA, adapted). Quest Motors, Inc., operates as a decentralized multidivision company. The Vivo division of Quest Motors purchases most of its airbags from the airbag division. The airbag division’s incremental cost for manufacturing the airbags is $90 per unit. The airbag division is currently working at 80% of capacity. The current market price of the airbags is $125 per unit.

Required:

1. Using the general guideline presented in the chapter, what is the minimum price at which the airbag division would sell airbags to the Vivo division?

2. Suppose that Quest Motors requires that whenever divisions with unused capacity sell products internally, they must do so at the incremental cost. Evaluate this transfer-pricing policy using the criteria of goal congruence, evaluating division performance, motivating management effort, and preserving division autonomy.

3. If the two divisions were to negotiate a transfer price, what is the range of possible transfer prices? Evaluate this negotiated transfer-pricing policy using the criteria of goal congruence, evaluating division performance, motivating management effort, and preserving division autonomy.

4. Instead of allowing negotiation, suppose that Quest specifies a hybrid transfer price that “splits the difference” between the minimum and maximum prices from the divisions’ standpoint. What would be the resulting transfer price for airbags?

22-23 Multinational transfer pricing, global tax minimization.

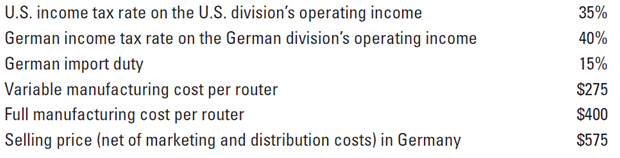

The Questron Company manufactures telecommunications equipment at its plant in Scranton, Pennsylvania. The company has marketing divisions throughout the world. A Questron marketing division in Hamburg, Germany, imports 100,000 broadband routers from the United States. The following information is available:

Suppose the United States and German tax authorities only allow transfer prices that are between the full manufacturing cost per unit of $400 and a market price of $475, based on comparable imports into Germany. The German import duty is charged on the price at which the product is transferred into Germany. Any import duty paid to the German authorities is a deductible expense for calculating German income taxes.

Required:

1. Calculate the after-tax operating income earned by the United States and German divisions from transferring 100,000 broadband routers (a) at full manufacturing cost per unit and (b) at market price of comparable imports. (Income taxes are not included in the computation of the cost-based transfer prices.)

2. Which transfer price should the Questron Company select to minimize the total of company import duties and income taxes? Remember that the transfer price must be between the full manufacturing cost per unit of $400 and the market price of $475 of comparable imports into Germany. Explain your reasoning.

22-24 Multinational transfer pricing, goal congruence (continuation of 22-23).

Suppose that the U.S. division could sell as many broadband routers as it makes at $450 per unit in the U.S. market, net of all marketing and distribution costs.

Required:

1. From the viewpoint of the Questron Company as a whole, would after-tax operating income be maximized if it sold the 100,000 routers in the United States or in Germany? Show your computations.

2. Suppose division managers act autonomously to maximize their division’s after-tax operating income. Will the transfer price calculated in requirement 2 in Exercise 22-23 result in the U.S. division manager taking the actions determined to be optimal in requirement 1 of this exercise? Explain.

3. What is the minimum transfer price that the U.S. division manager would agree to? Does this transfer price result in the Questron Company as a whole paying more import duty and taxes than the answer to requirement 2 in Exercise 22-23? If so, by how much?

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

Login | Sign Up

Login | Sign Up