Question 4

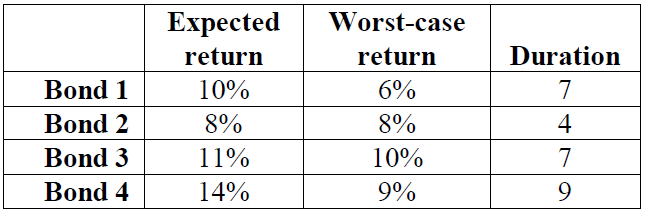

Linear programming models are used by many Wall Street and Bay Street firms to select a desirable bond portfolio for their clients. The following is a simplified version of such a model. TAL Private Investments has $1 million to invest for a client and is considering an investment in four bonds. The expected annual return, the worst-case annual return and the duration of each bond are given below. (The duration of a bond is a measure of its sensitivity to interest rate changes.)

TAL wants to maximize the expected return from the investment subject to three constraints that have been

placed on it by the client.

1) The worst-case annual return of the portfolio should be at least 8%

2) The average duration of the portfolio must be no more than 7. (For example, a portfolio that was made up of $600,000 in Bond 1 and $400,000 in Bond 4 has an average duration of [(600000 * 7) + (400000 *9)]/(600000 + 400000) = 7.8 It may also help you to recognize that 10x/ (10x + 15y) <= 5 can be rewritten as 10x<= 50x + 75y or 40x + 75y >=0).

3) At most, 45% of the portfolio can be in invested in a single bond.

a) Formulate a linear model that will help TAL make the portfolio composition decision. Be sure to define your decision variables clearly including the units of measure for each.

b) Solve the problem using Excel and Solver and submit a printout of your model as is done in Question 4 above.

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

Login | Sign Up

Login | Sign Up