Section A

Question 1

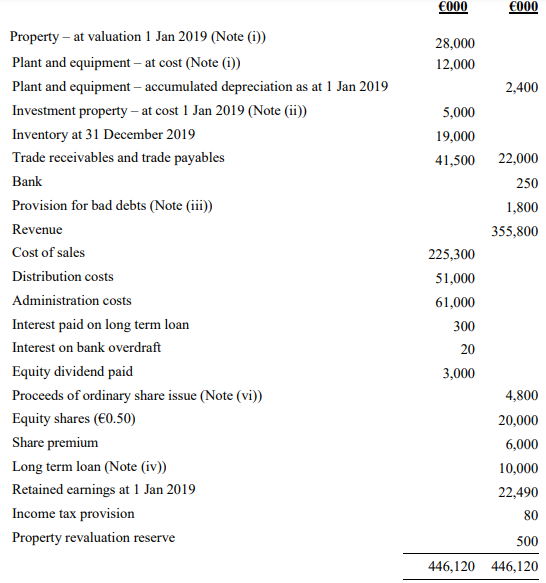

The following trial balance has been extracted from the financial records of Lightening Co as at 31 December 2019:

The following additional information is relevant:

(i) Non-current assets: The property has a remaining life of 40 years at 1 January 2019. The company policy is to revalue all property at each year end and at 31 December 2019 it was valued at €29 million.

All plant and equipment is depreciated at 20% per annum using the reducing balance method. Depreciation of all non-current assets is charged to cost of sales.

(ii) Investment property:

This property is held for its investment potential and meets the criteria of IAS 40 to be classified as an investment property. Lightening Co purchased this property on 1 January 2019 at a cost of €5 million. The agreed valuation as at 31 December 2019 is €5.5 million. The property has an expected useful life of 25 years from the date purchased.

(iii) Included in Trade Receivables is an amount of €500,000 relating to a customer who went bankrupt during December. This fact has only become known during the review of “Events After the Reporting Date” under IAS 10. Company policy is to make a provision for general bad debts equal to 5% of final Trade Receivables. All amounts in relation to bad debts should be included in cost of sales.

(iv) The long term loan of €10 million in the trial balance was received on 1 April 2019 and carries an annual interest rate of 6% per annum.

(v) The Directors have estimated the provision for income tax for the year ended 31 December 2019 at €3 million. The balance of income tax shown in the trial balance represents the over / under provision for the previous year.

(vi) During the year there was a 1 for 5 issue of ordinary shares at a premium of 20% to the nominal value. The directors are unsure how to record this and have lodged the cash into the bank and shown the proceeds as a single figure in the trial balance.

Required:

(a) Prepare the Statement of Comprehensive Income for the year ended 31 December 2019.

(b) Prepare the Statement of Changes in Equity for the year ended 31 December 2019.

(c) Prepare the Statement of Financial Position as at 31 December 2019.

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

Login | Sign Up

Login | Sign Up