Chapter 11:

Questions and Problems 9: Returns and Standard Deviations

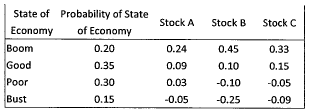

Consider the following information:

a. Your portfolio is invested 30 percent each in A and Cand 40 percent in B. What is the expected return of the portfolio?

b. What is the variance of this portfolio? The standard deviation?

Questions and Problems 16. Using CAPM

A stock has a beta of 1.13 and an expected return of 12.1 percent. A risk-free asset currently earns 5 percent.

a. What is the expected return on a portfolio that is equally invested in the two assets?

b. If a portfolio of the two assets has a beta of 50, what are the portfolio weights?

c. If a portfolio of the two assets has an expected return of 10 percent, what is tis beta?

d. a portfolio of the two assets has a beta of 2.26, what are the portfolio weights?

How do you interpret the weights for the two assets in this case? Explain

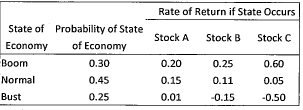

Questions and Problems 22: Portfolio Returns and Deviations

Consider the following information about three stocks:

a. If your portfolio is invested 40 percent each in A and B and 20 percent in what is the portfolio expected return? The variance? The standard deviation?

b. If the expected T-bil rate is 3.80 percent, what is the expected risk premium on the portfolio?

c. the expected inflation rate is 3.50 percent, what are the approximate and exact expected real returns on the portfolio? What are the approximate and exact expected real risk premiums on the portfolio?

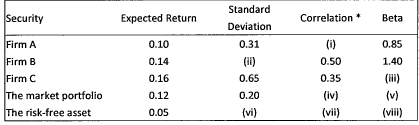

Questions and Problems 29: Correlation and Beta

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table.

b. Is the stock of Firm A correctly priced according to the capital asset pricing model (CAPM)? What about the stock of Firm B? Firm C? If these securities are not correctly priced, what is your investment recommendation for someone with a well-diversified portfolio?

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

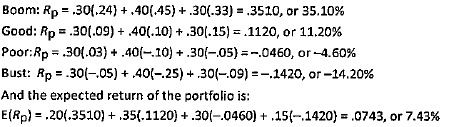

a. This portfolio does not have an equal weight in each asset. We first need to find the return of the portfolio in each state of the economy. To do this, we will multiply the return of each asset by its portfolio weight and then sum the products to get the portfolio return in each state of the economy. Doing so, we get:

Login | Sign Up

Login | Sign Up