Problem 1

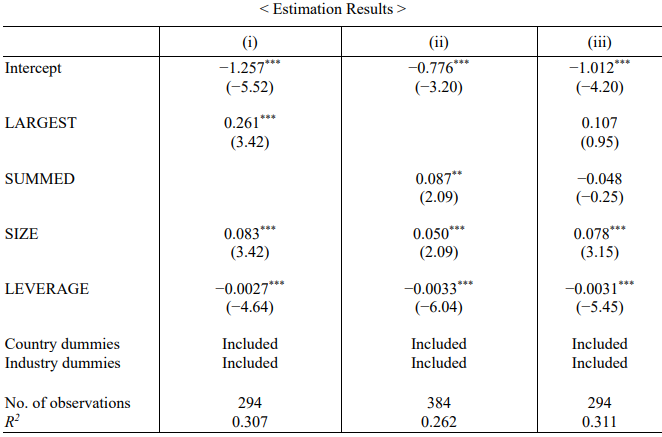

Mitton (2002) analyses firm-level data from the five East Asian crisis economies of Indonesia, Korea, Malaysia, the Philippines, and Thailand to study the impact of corporate governance on firm performance during the Asian economic crisis. To measure firm performance during the crisis, he uses stock returns over the crisis period, from July 1997 through August 1998. To assess the impact of corporate governance variables on firm stock price performance during the crisis, he estimates the following model:

One aect of corporate governance studied here is ownership concentration. As a measure of it, he considers two measures of ownership concentration. The first is the ownership percentage (in terms of cash flow rights) of the largest shareholder in the firm, which is named as LARGEST. The second is the total holding of all shareholders that own 5% or more of the stock, which is named as SUMMED.

(a) The corporate governance variables LARGEST and SUMMED are significant factors when they are included separately, as shown in columns (i) and (ii). However, column (iii) shows that the coefficients for the two variables become insignificant when they are included together. Explain why this can happen.

(b) The note to the table says that "White's heteroscedasticity-consistent t-statistics" are given in

brackets. Explain what it means.

Students succeed in their courses by connecting and communicating with an expert until they receive help on their questions

Consult our trusted tutors.

Login | Sign Up

Login | Sign Up